-

82% of Nubank's active loan customers were ineligible to take a second loan. Among the 18% who were eligible, most weren't converting either.

I led the design exploration and validation of new loan concepts, helping reframe the experience from “extending debt” to enabling access to additional funds in a way users could understand and feel confident about.

-

Lower-than-projected conversion confirmed the hypothesis: the barrier to loan recurrence is psychological, not structural. No amount of UX polish overcomes a deep-seated emotional association with debt.

This shifted the team's strategic roadmap from "how do we make the offer clearer" to "how do we change the relationship users have with their loan over time."

-

By surfacing the gap between system logic and user psychology, I shifted the team's understanding of what "recurrence" actually requires. The product had been optimizing for eligibility and offer clarity.

The real lever was timing and emotional framing, and proving that changed our roadmap. Future lending strategies at Nubank incorporated perceived progress and loan lifecycle positioning as first-class design variables.

Top Up Loans

— The ProblemLoan recurrence in Brazil carries a strong stigma, driven by high interest rates and the fear of falling into long-term debt.

At the same time, there was a clear mismatch between user demand and system constraints. While many users showed interest in accessing more credit, 82% of active customers were blocked by eligibility rules.

Key Challenges

-

Users approached loans with caution, often influenced by fear and past experiences.

— Emotional weight of borrowing

-

Increasing conversion could not lead to higher delinquency or irresponsible borrowing.

— Risk-sensitive environment

. Design Process

. Design Process

Our research revealed that completing a loan wasn't just a financial event, it was an emotional milestone. Users experienced it as closure. Asking them to immediately take a new loan felt psychologically equivalent to undoing that progress.

The product was treating loan recurrence as a financial decision. Users were experiencing it as an identity decision: am I someone who has their debt under control, or not?

Behavior and perception

How might we offer additional credit in a way that aligns with how users perceive financial progress and control?”

Opportunity framing

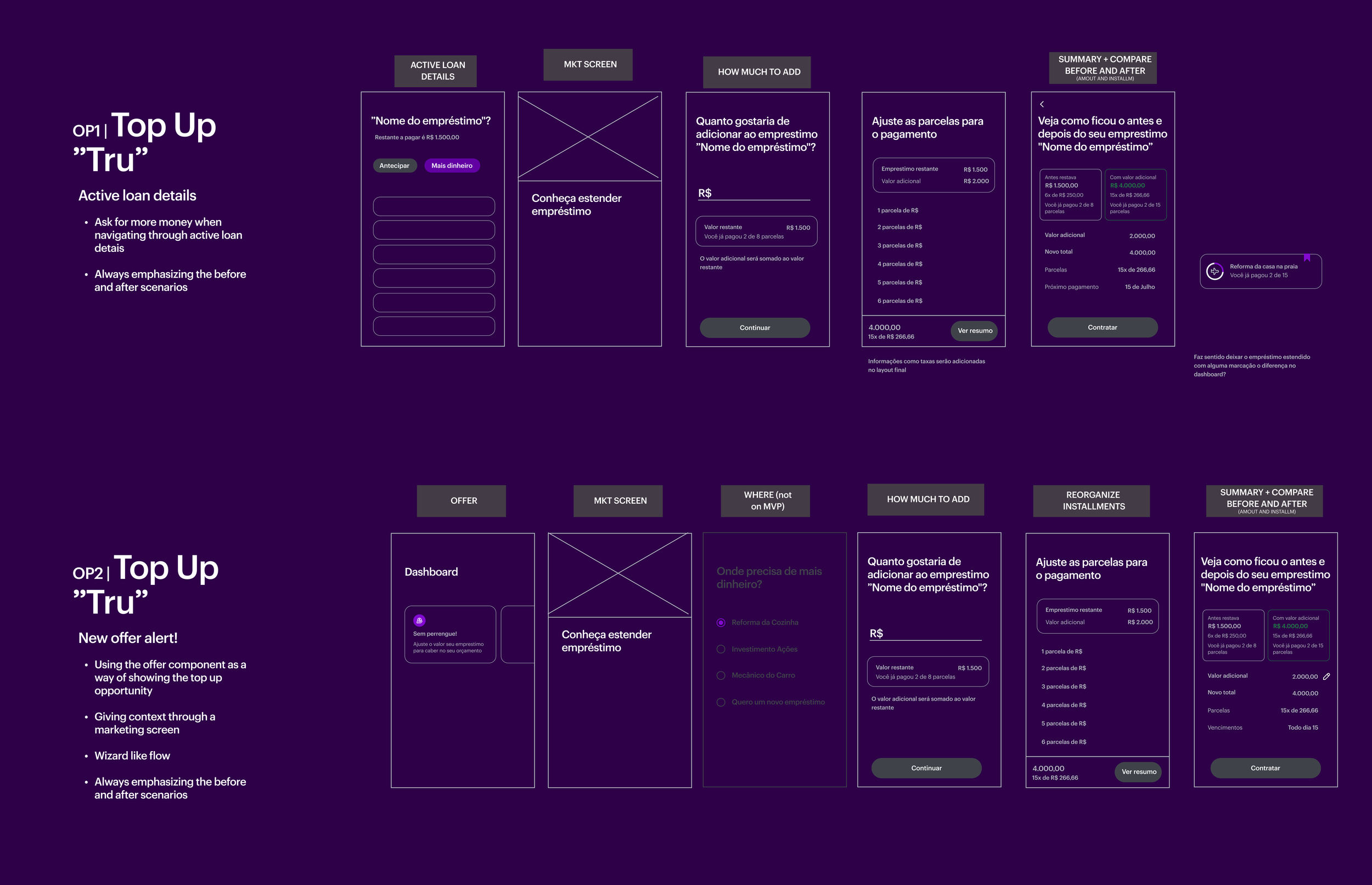

We explored multiple concepts focused on reframing both entry point and experience.

Two key directions emerged:

Positioning the offer as access to additional money rather than debt extension

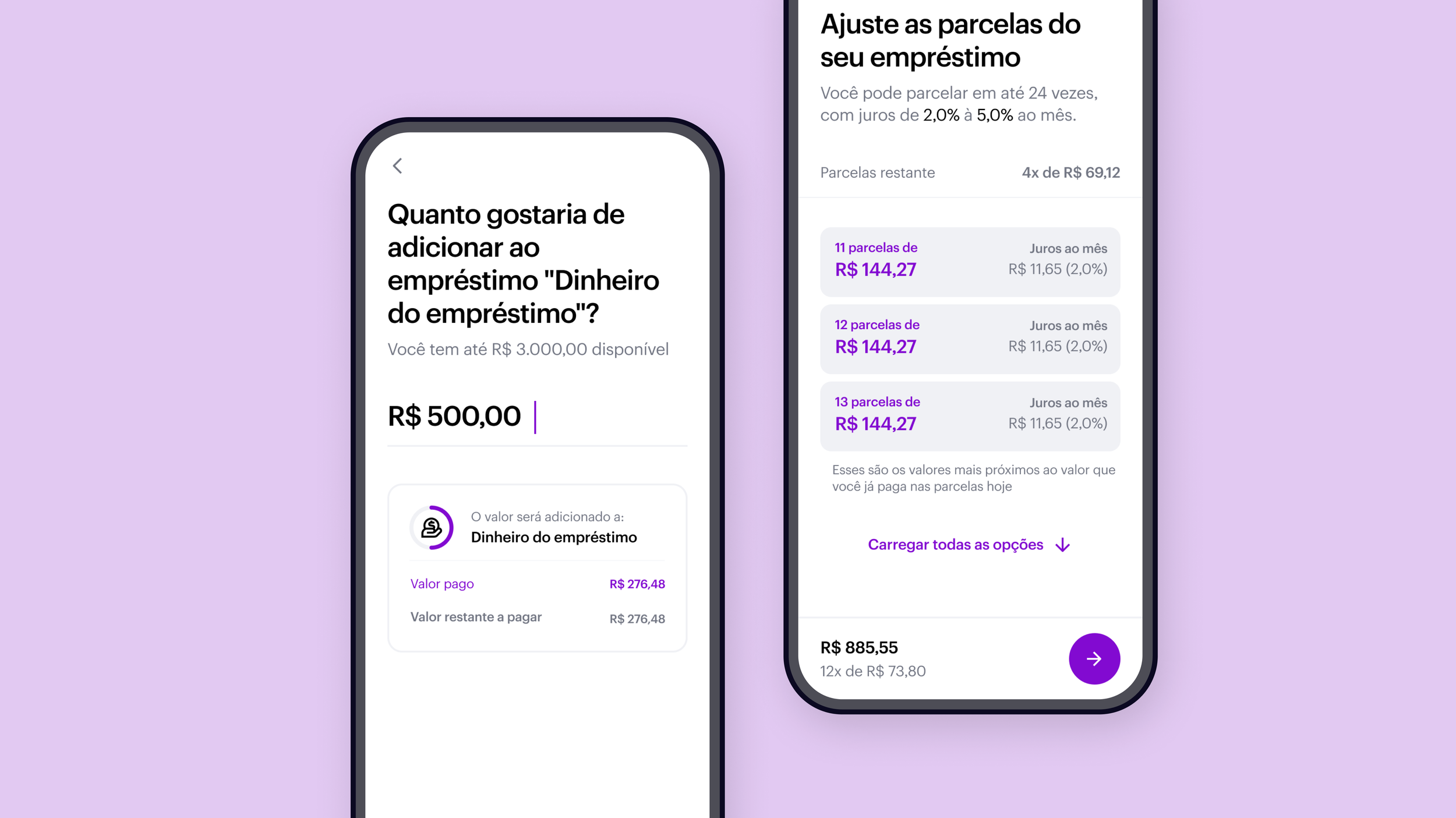

Introducing flexibility in repayment by delaying second-loan installments

Concept explorations

We tested different framings and flows through experiments and usability testing.

Key insights included:

strong engagement when framed as “more money”

high rejection when framed as “extend your loan”

emotional drivers played a larger role than purely financial logic

Validation focused not only on conversion, but on whether users understood and trusted the experience.

Validation

The final approach combined behavioral framing and structural flexibility.

Instead of presenting a loan extension, the experience introduced a new credit opportunity

— Key directions included:Aligned with user intent (access to money)

Preserved a sense of financial progress

Provided clarity on repayment and outcomes

Impact

On Business

The experiment did not hit adoption targets, and that was the finding.

Lower-than-projected conversion confirmed the hypothesis: the barrier to loan recurrence is psychological, not structural. No amount of UX polish overcomes a deep-seated emotional association with debt. This shifted the team's strategic roadmap from "how do we make the offer clearer" to "how do we change the relationship users have with their loan over time."

That's a more expensive problem to solve, and a more valuable one to have identified.

Design

By surfacing the gap between system logic and user psychology, I shifted the team's understanding of what "recurrence" actually requires. The product had been optimizing for eligibility and offer clarity.

The real lever was timing and emotional framing, and proving that changed our roadmap. Future lending strategies at Nubank incorporated perceived progress and loan lifecycle positioning as first-class design variables.